Imagine you are a lawyer working long hours at a demanding job with the aim of saving a nice nest egg by age 45. Then you do something you’ve always been passionate about – teach high school, or work for a non-profit until retirement at 65. The net worth accumulated when you were a lawyer will sustain you in your retirement years. But until then, you make enough money to live comfortably and do something you are passionate about without the stress and long hours of Big Law.

Does this sound appealing to you? You may want to consider coasting into FIRE. Plan your strategy for Financial Independence/Retire Early (FIRE) with our FIRE calculator.

Plan your strategy for Financial Independence/ Retire Early (FIRE) with our FIRE calculator.

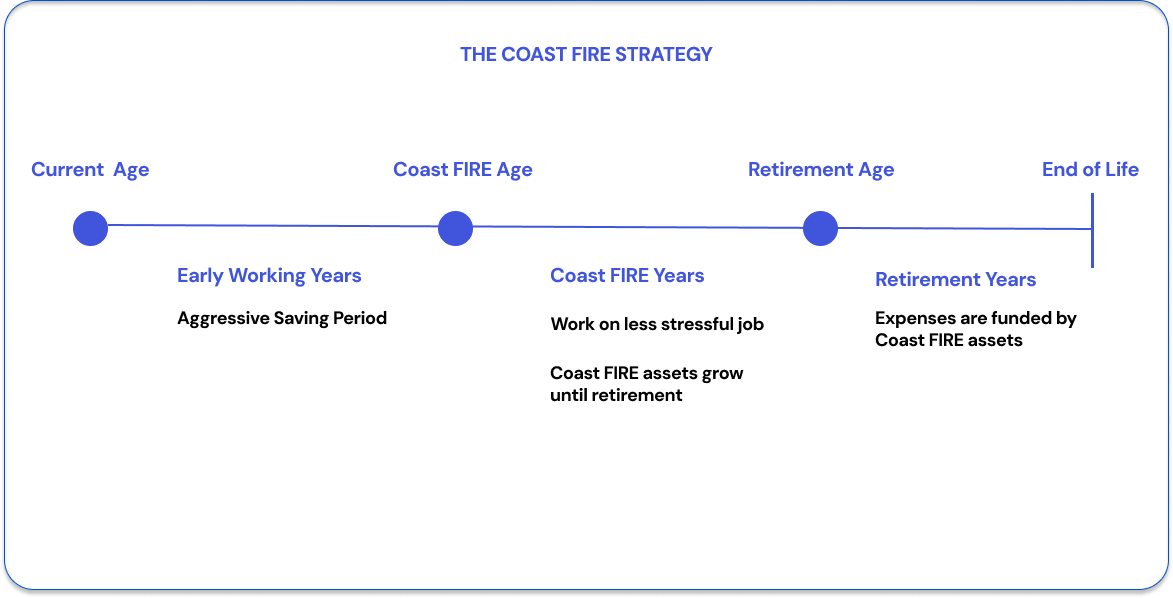

The Coast FIRE approach focuses on saving aggressively early in your career and accumulating assets that enable you to retire at the standard retirement age, say 65, and then working on a job that is less stressful or something you are passionate about until the actual age of retirement. This ensures that you do not have to be extra frugal to retire early and potentially live frugally in retirement as well, but instead have a reasonably comfortable lifestyle leading upto and into retirement.

With COAST FIRE, you save aggressively in the early stages of your career, until you get to a point where you have saved enough for retirement at the standard retirement age. Then you ‘coast’ until retirement, and do not save as much as before or even nothing until you retire. You are just paying for your current expenses without saving as much as before, because you have already saved enough for retirement. After retirement, the nest egg you built during your early aggressive saving years will sustain you through your retirement years.

The Financial Independence, Retire Early (FIRE) method requires that you build enough assets to retire early and live on your accumulated assets for the rest of your life. This means you have to be very frugal in your working years and manage your expenses in retirement such that your money lasts your entire lifetime after your early retirement. FIRE practitioners plan to stop working once they hit their FIRE age and leave the workforce.

Coast FIRE is a bit different. With COAST FIRE, you save aggressively and build enough assets early on. But your assets can grow and compound until the standard retirement age, which is when you retire. You will work from your Coast FIRE age until the standard retirement age, but at a less demanding job or something you are passionate about but may not pay as much. And this is fine because you have already saved enough for your retirement years early on. This means you do not leave the workforce after you hit the Coast FIRE age, but keep working, but just not saving as aggressively as before.

The goal of Coast FIRE is to achieve financial security and build assets at a younger age, and then having the freedom to work only as much as is needed to pay for current expenses without having to save aggressively for future retirement, since you already have saved enough for retirement in your early working years.

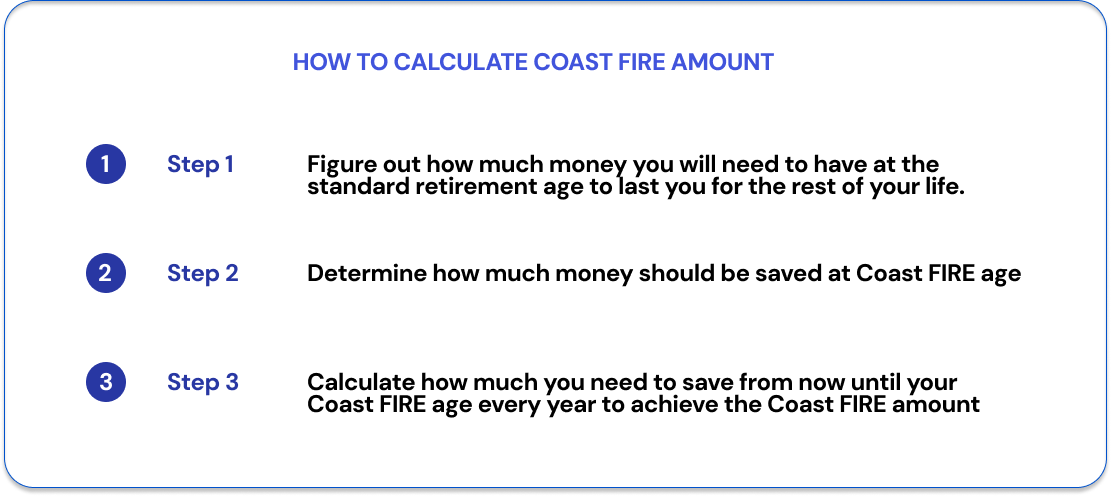

You can plan your Coast FIRE strategy in 3 steps:

In Stage 1, you save aggressively and as much as possible to sustain you in your future retirement years. Your goal is to achieve your Coast FIRE number, and the assets you save will compound from the Coast FIRE age until retirement age.

At this stage, you are still working, but have the financial freedom to work at a more fulfilling or less demanding job that may not pay as well. You may even be able to go part time. At this stage you just need to earn enough to pay your living expenses, but you do not need to save as much as before.

In parallel, the nest egg you built during your working years will grow and compound until the age of retirement. You do not touch any of this money, but live on the earnings from your current job to sustain you through these years.

You retire at a normal retirement age, say in your 60s, and use the nest egg saved until your Coast FIRE age to help you through your retirement for the rest of your life. These assets have compounded from the time you achieved Coast FIRE until retirement age and you now have enough to last you for your lifetime.

Here are the steps needed to calculate your Coast FIRE number along with an example to make it easy to understand.

Let us say you are 28 years old, and starting your career. You hope to achieve Coast FIRE at age 40 and want to spend the years from 40 to 65 working on something you are passionate about.

Step 1: Figure out how much money you will need to have at the standard retirement age to last you for the rest of your life.

Let us say that you anticipate expenses of $100,000 per year in retirement after age 65. Using the 4% withdrawal rule, you should have saved $100,000/0.04 = $2,500,000 at the age of 65.

Step 2: Determine how much money should be saved at Coast FIRE age

You should have saved enough money at Coast FIRE age to compound to $2.5M by age 65. A key factor here is the rate of return. The higher the expected rate of return, the lower is the Coast FIRE amount. Of course, it is important to take into account that a higher rate of return is correlated with higher risk.

So by age 40, our 28 year old should have accumulated $582K, assuming a 6% annual rate of return.

Step 3: Calculate how much you need to save from now until your Coast FIRE age every year to achieve the Coast FIRE amount.

In our example, with a starting age of 28, you need to put aside about $34,000 every year to achieve $582K by age 40. This is an aggressive savings goal in your early career years, but if you can sock away this amount by maxing out your 401K, Roth IRAs and by saving some money in brokerage accounts, you can achieve this goal.

Of course, this also means that you need to have a job that allows you to earn and save so much. If this is too aggressive, consider Coast FIRE age of 45. In this case you will need to have accumulated $770K by age 45 and need to save $27,000 every year from now until 45 to achieve this.

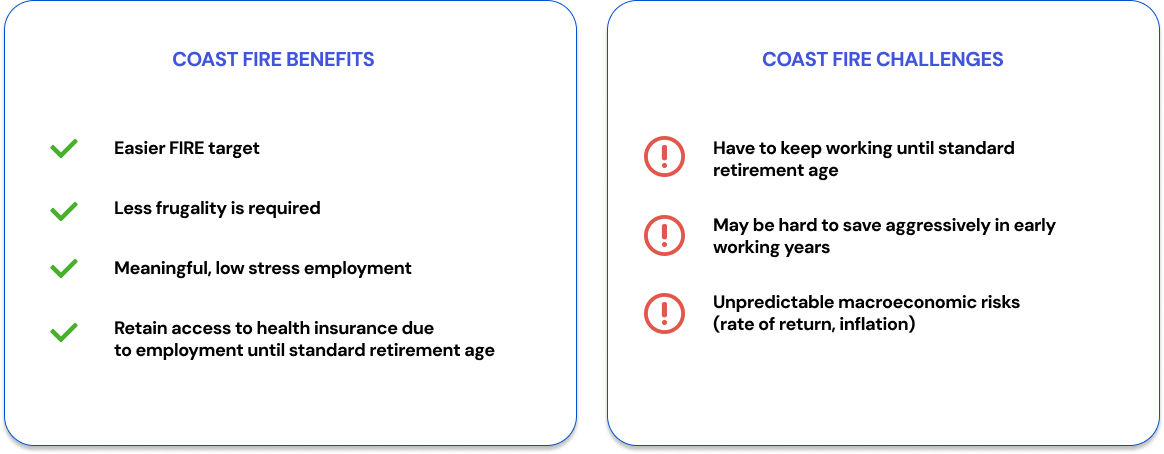

A Coast FIRE approach does not demand as aggressive a savings strategy as regular FIRE. This is due to 2 reasons (1) The retirement age is typically in one’s 60s, so your money has longer to compound and (2) Even if you are working a less demanding job between your Coast FIRE age and retirement age, this income is used to fund your lifestyle and you do not have to dip into your Coast FIRE savings to fund it.

Since the Coast FIRE target amount is typically lesser than the FIRE target amount, a Coast FIRE approach demands less frugality. This takes the pressure of having to save super aggressively and live very frugally in your peak earning years. Thus, you can still enjoy a nice lifestyle while also saving aggressively.

Once you attain Coast FIRE, you can work on something that you are passionate about, or switch to a job or profession that is less stressful. Some people may choose to work part time or take more vacations. In general, you can have a more relaxed working life with more work-life balance and focus on other aspects of your life.

You just need to make sure that you can support your lifestyle without dipping into the Coast FIRE savings which are allocated for retirement years.

With Coast FIRE, you will still likely work, albeit in a less demanding role. So you will likely have access to health insurance or other employment benefits even though you may not be working or saving as aggressively as before. This can reduce a lot of stress and pressure that one may encounter if you were to fully retire (as is the case with the FIRE approach).

Coast FIRE demands that you still keep working from your Coast FIRE age until the standard retirement age in the 60s. So you won’t have the freedom to completely quit work and pursue other hobbies or interests.

Typically, people tend to earn less earlier in their careers and then earn more as they gain more experience. With this approach, you have the pressure of saving aggressively in your early working years, when your income is likely to be lower.

Another related problem is that people tend to make the most money in their peak working years. But with Coast FIRE, this is when you step back from a demanding career to work on something less demanding. So you risk losing out on peak earning years in which you may choose to step off the career pedal.

There are many years between Coast FIRE and actual retirement, but the assets you have saved until Coast FIRE will compound until retirement and tide you over for retirement years. This brings macroeconomic risks into the equation.

If the return on investment on assets turns out to be lower than expected, you may not be in a position to retire as planned.

Similarly, inflation may impact returns or require you to spend more than expected in retirement to support a similar lifestyle. This means that the amount you have saved will not be enough for retirement needs.

The Coast FIRE approach can be a happy medium for people who want financial independence but keep working until retirement age. The Coast FIRE lifestyle also affords more work-life balance. This is a good option when one does not want to live an extreme frugal lifestyle and prefers to enjoy life a bit in the working years while also saving aggressively for retirement. The Coast FIRE method avoids the extreme frugality of the FIRE approach while also ensuring that one enjoys one’s working years without being completely consumed by work. If you prefer an even higher spending approach, you might consider the Fat FIRE strategy.

Planwell is building a fully automated AI financial planner that helps users plan for financial independence and early retirement.

To help you further in your journey, check out some of these helpful resources:

Attributions: