House hacking is the act of generating income from your home or real estate property while living in it. This can be done by renting out a part of the home you live in, or renting out multiple units of a multi-family unit while living in one of them. House hacking can also be done through short term rentals such as Airbnb or Vrbo. House hacking helps pay for part or all of the mortgage or housing expenses, thereby making real estate investment more attractive.

Read our blog post: How Much Home Can I Afford?

House hacking works as follows: You buy a single family or multi-family unit and rent out some or all of the property. The tenant pays rent and also sometimes shares the utilities bills, thereby reducing living expenses for the property owner. This generates cash flow and passive income that makes the real estate investment more affordable, enables you to generate cash flows and improves the return on the investment.

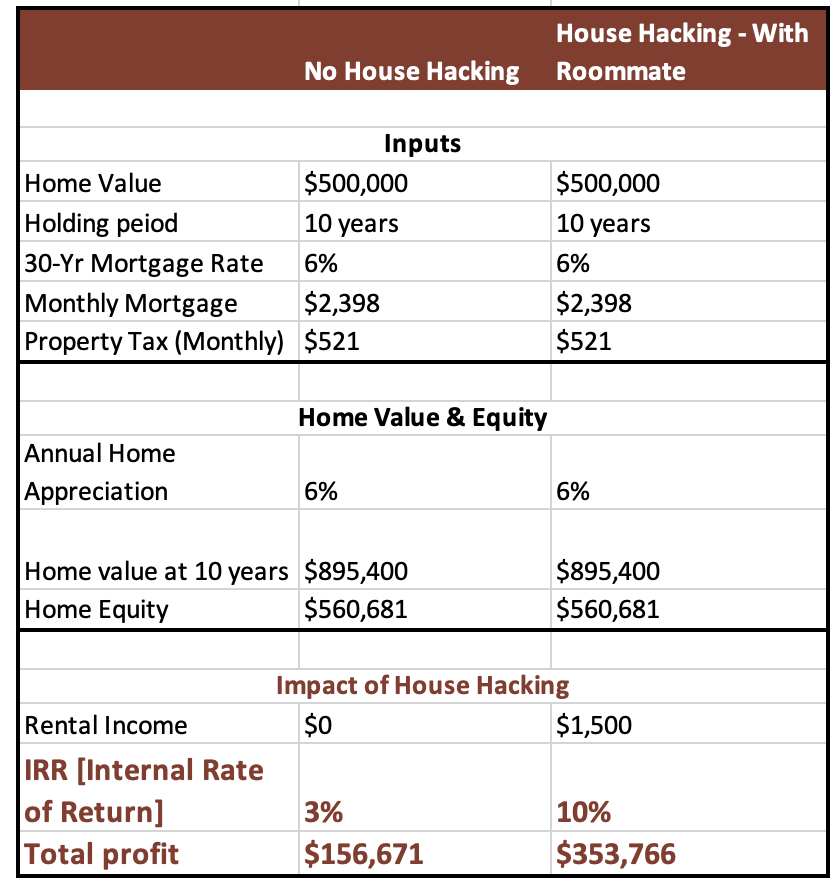

Let us assume the following scenario:

As you can see, house hacking makes the investment significantly more attractive through generating rental income.

You can increase your home affordability and ROI by getting a roommate whose rent pays part of the mortgage and utilities.

Pros

Cons

Buying a rental, multi-family property is a good way to generate passive rental income while not having to share living spaces with strangers. You can live in one of the rental units and rent out other units.

Pros

Cons

Increasingly, these days, people are renting out their homes as short term rentals on Airbnb or Vrbo. This helps them pay part of the mortgage while not having to deal with long term roommates. This may be especially useful to people who travel often and want to monetize their property when they are not using it.

Pros

Cons

You may have heard of house flips, in which you buy a property that is not in great condition, and then upgrade/ remodel it and sell for a profit. There is another take on this concept. While you are remodeling the house, you can live in it, thereby not having to pay a mortgage or rent anywhere else. Then after a few months, you sell this property for a profit and move on to a new one and repeat the process.

Pros

Cons

House hacking can enable you to afford a home that you may not have been able to otherwise afford. The rent from house hacking may help pay for part of the mortgage or even the entire mortgage.

House hacking helps generate cash flow through rental income. Additionally the renter may also share in the utility bills, further helping you save money.

House hacking can improve the return on investment on the real estate investment. This is through additional cash flows which offsets the mortgage and other expenses of home ownership.

While renting out part of the home or the entire home, you will simultaneously build home equity over time. House hacking enables you to afford a home, and you can build equity. With adequate price appreciation, you can make a profit on the home as well at the time of selling.

House hacking is a lower risk way to start on the path to real estate investing. The additional cash flows reduce the barrier to home ownership and by making a profit on the sale of the first home, you can use this as capital to invest in subsequent real estate properties. Moreover, you also learn the basics of managing tenants and renters.

To succeed with house hacking, it's essential to thoroughly understand and plan for all costs, responsibilities, and regulations that come with managing a rental property.

House Hacking helps you generate income and cash flow from your house while living in it. It helps generate a higher rate of return on the real estate investment. However, you may have to deal with the inconvenience of having a stranger live in the house and managing real estate property, so it may not be for everyone.

See our blog posts related to home buying and real estate.

How much house can I afford with my salary?

How much house can I afford on a $200,000 salary?

How much house can I afford with a $100,000 salary?

How much house can I afford with $80,000 salary?

How much house can I afford with $60,000 salary?

Photo by Hugo Sousa on Unsplash