The Boglehead Investment Approach

Designed by Freepik

Jack Bogle was the founder of the index investing powerhouse Vanguard and a proponent of low-cost index investing for everyone, not just financially savvy or wealthy individuals. His investment philosophy has achieved cult status and the followers of his low-cost and long-term investing approach are called Bogleheads. He wrote the all time bestseller The Bogleheads’ Guide to Investing, the definitive guide to personal finance and investing.

What is the Boglehead Investing Strategy?

Jack Bogle’s investment philosophy is simple yet effective. It emphasizes investing in low investment fees funds, asset diversification and reducing volatility with prudent risk management. The objective of ‘Bogleheads investing’ is to get rich slowly but steadily.

Key Principles of Boglehead Investing

Let us first start with some definitions:

Active investing is the process of trading actively by buying and selling stocks with the aim of exceeding returns of the markets or a stock index. Often, a fund manager will analyze stocks to make buy and sell decisions. Active investment is usually associated with market timing and higher fees.

Passive investing is a long-term investing strategy that is executed by buying stocks and holding them for a long time. Passive investors are not seeking to time the market and want to match market returns instead of exceeding them. Passive investing requires less management and lower frequency transactions and therefore is associated with low fees and low transaction costs.

Bogleheads Emphasize Passive Investing

As you might imagine for a movement founded by Jack Bogle, the pioneer of index investing, the Bogleheads investing strategy strongly recommends passive investing in order to reduce investment fees and transaction costs. Moreover, timing the market can lead to investment losses due to emotional decision making.

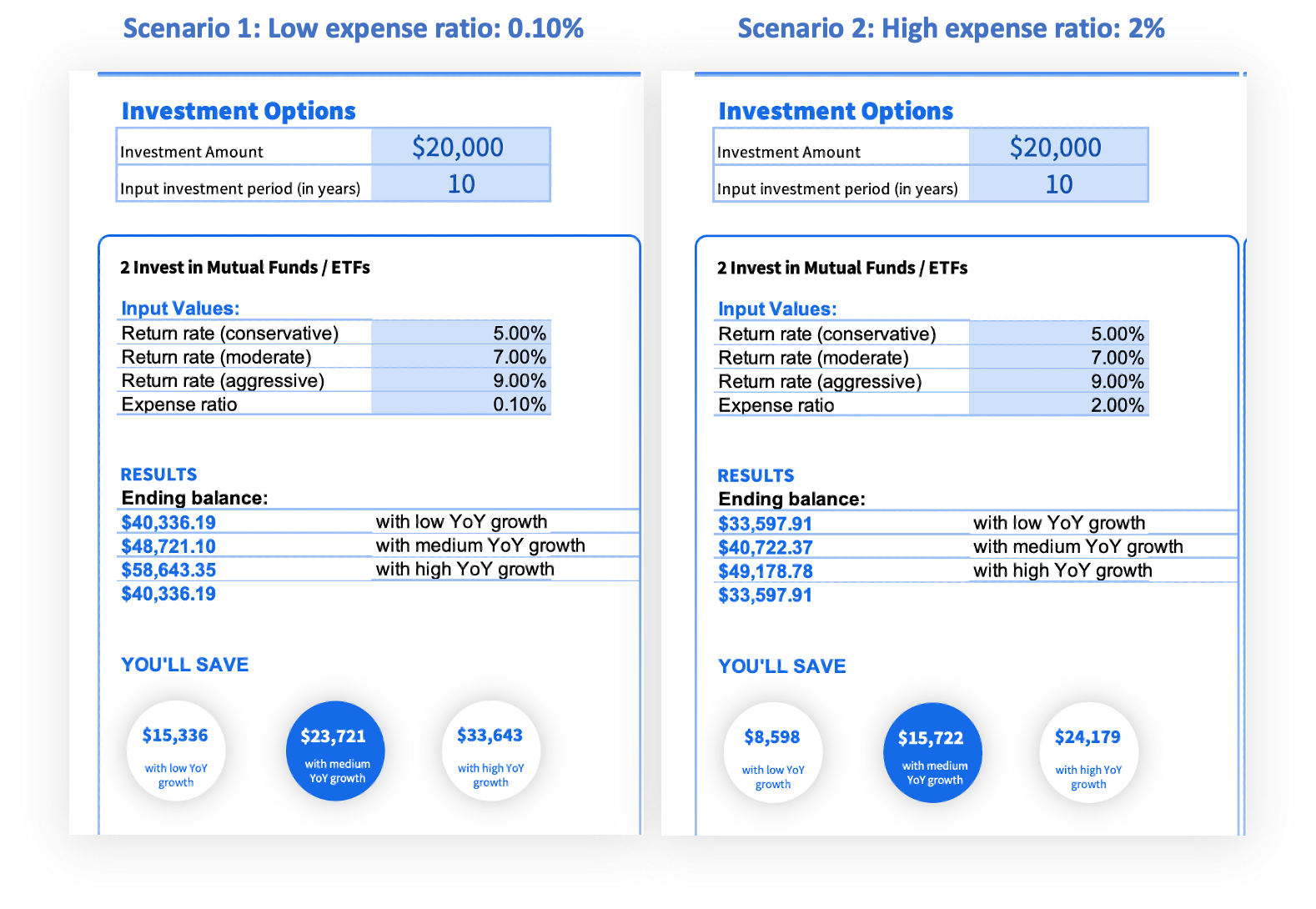

Let us look at an example of how investment fees can reduce returns. Assume you have $25,000 and you invest this for a period of 10 years. We look at how this money grows in low, medium and high growth scenarios.

Scenario 1: Passive investing, with expense ratio of 0.10%

After 10 years your initial investment of $25,000 is worth as follows in a low expense ratio scenario of 0.10%

Low growth scenario: $ 40,336

Medium growth scenario: $48,721

High growth scenario: $58,643

Scenario 2: Active investing, with expense ratio of 2%

After 10 years your initial investment of $25,000 is worth as follows in a high expense ratio scenario of 2%

Low growth scenario: $33,591

Medium growth scenario: $40,722

High growth scenario: $49,178

As you can see, even with all other factors such as investment growth rates being equal, you see higher returns with a low expense ratio scenario.

Manage risk and volatility

The Bogleheads approach emphasizes the importance of risk management and reducing volatility. Asset diversification is a good strategy to reduce volatility. Investing in market-tracking index funds or total market index funds are an effective way to reduce volatility, achieve diversification and keep fees low.

Another key principle of diversification is to manage asset allocation by putting money in different asset classes, including stocks, bonds, cash, real estate and so on. It is usually recommended to invest more aggressively when you are young and have time to recoup any investment losses, and shift more and more assets into less risky investments as you get closer to retirement.

Tax Efficiency is important.

The biggest expense for most people is not housing or travel or dining out. It is taxes. And this is not an expense that you can choose to skip.

However, investing in tax advantaged retirement accounts can help you save on taxes while making sure you save consistently for retirement. Tax advantaged retirement funds include 401Ks, IRAs and Roth IRAs.

With 401K and IRAs, you invest pre-tax dollars and pay taxes on contributions and withdrawals at the time of withdrawal during retirement. This reduces your taxable income for the current year and thereby reduces your tax bill. Additionally, you will also benefit if your company offers a 401K match.

Roth IRAs work differently. You pay taxes now, but withdrawals are tax free, with certain conditions.

Start investing early

The sooner you start investing, the more time your money has to compound and grow. This advice is especially relevant to young adults for whom age is on their side.

Slow and steady investing for the long term

Invest a steady amount periodically, ideally every month. You can follow approaches such as Dollar Cost Averaging (DCA) which enables you to invest a fixed amount every month. You buy more stock at lower prices and less stock at higher prices. This disciplined approach to investing reduces volatility and avoids the temptation to time the market.

You can use our Financial Independence Calculator to calculate how much you need to save to achieve your retirement and financial independence goals.

Who is the Bogleheads Investing Approach Right For?

Warren buffet famously said that upon his death, the trustee of his wife’s inheritance was instructed to put 90% of her money into a very low-fee stock index fund and 10% into short-term government bonds. If the world’s best active investor is recommending low cost index funds for his wife, then this approach should certainly work for the rest of us!

The Boglehead investing approach is applicable to almost anyone, especially the average person. It does not require inherited wealth, a trust fund or specialized financial knowledge. All that is needed is some discipline and a willingness to think long term.

This means that this approach is particularly helpful for certain types of people:

- Busy individuals who would prefer to set their investing on auto-pilot with dollar cost averaging, and buy and hold stocks for the long term. These folks may wish to focus on their careers rather than spend time researching stocks and trading actively.

- People who are disciplined with their savings and investing, and avoid constant trading and timing the market.

- Non-emotional investors: Boglehead investors do not get carried away by the ups and downs of the market but continue to invest diligently, diversify their asset allocations and rebalance their portfolios without panicking.

Who may the Bogleheads Investing Approach not be Right For?

As we said before, pretty much everyone is the right candidate for Bogleheads investing. However, some people may not appreciate this investment philosophy for the following reasons and may wish to pursue more active investing.

- People who love to do investment research by themselves and have the time to spend on this research. If you are passionate about learning about stocks and markets and like to spend your free time researching these topics, you may wish to take a more active approach and be your own fund manager.

- People interested in more unconventional and alternative investments: If you adopted the Boglehead investing approach in its entirety, you may have missed investing in crypto or angel investing or other alternative investments. While these are decidedly riskier investment options, some folks may wish to maintain a portfolio of their assets in alternative or riskier investments with the hope of generating much higher returns than the market average.

- People with high net worth may prefer to get white glove investment advice from family offices and specialized investment firms.

For everyone else, there is the Boglehead Investing approach.

Conclusion

The Bogleheads Investing Approach is a disciplined approach to getting rich slowly through low cost index fund investing, asset diversification and avoiding frequent trading and market timing. This approach encourages investing in tax advantaged funds and taking the long view to building wealth.

Read our top blog posts to get more financially savvy:

- Top 5 Books to Learn Financial Literacy: The first book on the list is Jack Bogle’s The Bogleheads’ Guide to Investing, of course!

- How to Use AI Budget Calculators and Tools to Plan Your Finances: Take advantage of our free FIRE calculator to plan your finances more effectively.

- Will AI replace financial advisors? Find out!

- What is Coast FIRE? Find out how to Coast Your Way to Financial Independence.

- How to retire early and achieve financial independence: Tips to retire early and achieve FIRE (Financial Independence, Retire Early)

- How to build a personal financial plan: Before you make a home purchase, make sure to build your personalized financial plan with our 10 step guide.

- 5 Common Money Mistakes to Avoid: Learn about the pitfalls that could derail your early retirement plans.

- Top 5 Books to Learn Financial Literacy: The first book on the list is Jack Bogle’s The Bogleheads’ Guide to Investing, of course!

Image credit: Created by Freepik

Related Posts

About

©2023 Planwell.io