Not everyone wants to work all the way until their mid-60s before they retire. Perhaps you are one of them and would like to retire early, say by age 55, so that you are still young enough to travel or pursue other interests. So how do you go about figuring out how much you need to retire early at 55?

Here is our step-by-step plan to get on track to retire early at age 55.

If you’re wondering how to retire early, especially by the age of 55, you’re not alone. Many people seek financial freedom before the traditional retirement age. But how do you know if it’s possible, and how much do you need to retire early without sacrificing your lifestyle? Use our free FIRE calculator to figure out how much you will need to have in assets to retire at age 55.

Enter basic financial information: You have to enter your gross income (before taxes), retirement contributions (401K, IRAs, etc), taxable savings in brokerage accounts, and balances you have saved so far.

Set your retirement goals: Enter your target retirement age of 55. Also think about your expense level and lifestyle post-retirement.

Review and edit assumptions such as rates of return before and after retirement, inflation and wage growth.

Results: You will be able to determine if you can retire by age 55 and how much money you need to save to retire at this age.

Let’s explore two different scenarios that illustrate how you can adjust your saving habits to retire at 55. These examples show how much you need to retire early depending on your lifestyle and savings plan. Let us model out some hypothetical scenarios to make sure you can retire at 55.

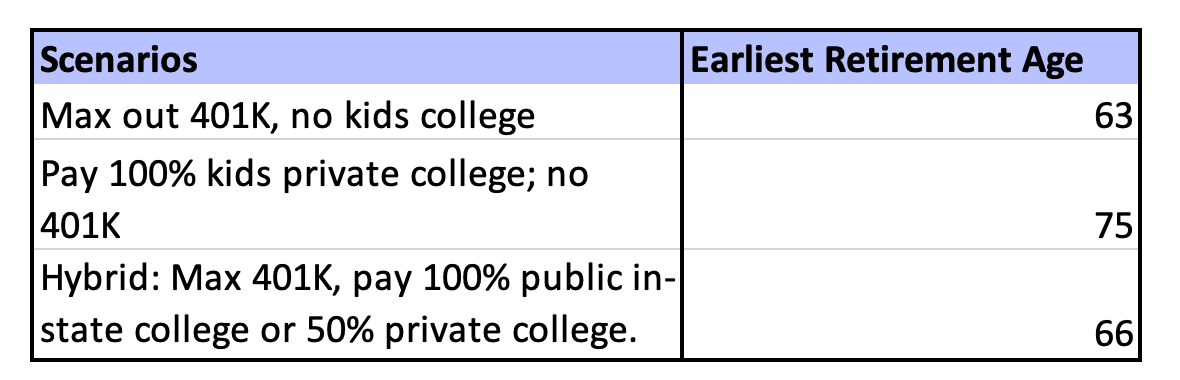

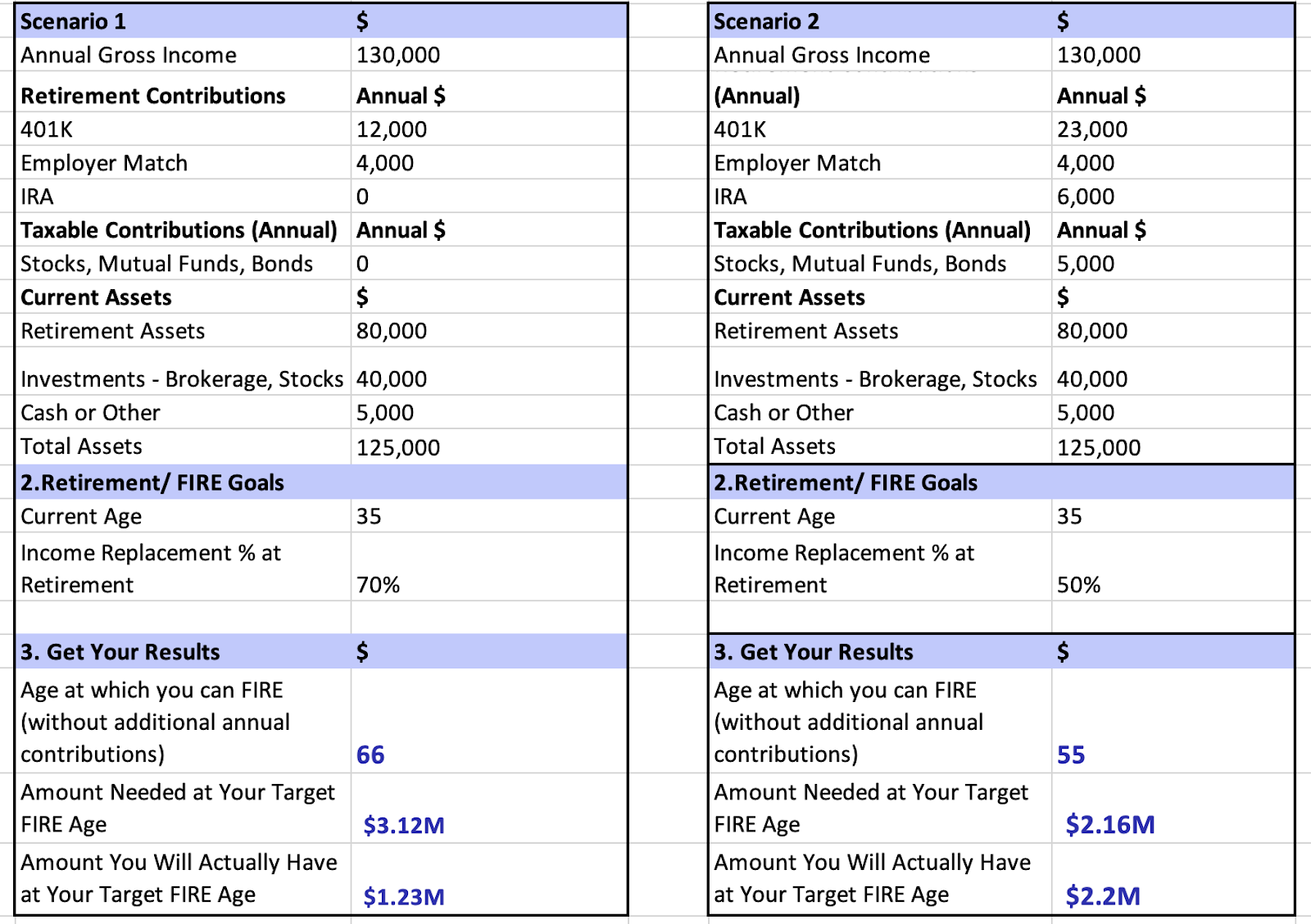

Scenario 1: A person aged 35 sets aside just $12,000 in their retirement savings every year. They already have saved up assets of $125,000. In retirement, this person maintains a lifestyle that requires them to live on 70% of their current income.

o Result: The earliest age they can retire is age 66.

Scenario 2: The same person maxes out their 401K with $23,000 in annual contributions and puts aside $6000 in IRA. In retirement they live more frugally at 50% of their current income, following a LeanFIRE approach to minimize expenses.

o Result: They can retire at age 55.

Assumptions: 7% return on assets before retirement and 5% after retirement.

You can play around with different scenarios and find out how to achieve your retirement goals with our free FIRE calculator.

The biggest factor that will help you is to save as much as possible, especially in tax-advantaged funds like 401Ks or IRAs. Max out your 401K if possible and make sure to get your employer match. Create a budget based on your savings goal and track your progress towards the goal.

While it may seem hard to stick to a budget and be frugal, it may be a good idea to really splurge on the things that you care about and cut back on everything else. This will ensure that you get to enjoy your life on the way to retirement, while also saving enough to retire early.

Do you have opportunities to increase your income by getting a raise or a new job? Alternatively think about opportunities for earning side income using skills you may already have, such as house hacking. Make sure to use all the increased income towards savings instead of indulging in lifestyle creep.

A big factor that drives whether you can retire at age 55 is the type of lifestyle you want to maintain in retirement. If you have paid off your mortgage, you may have lower expenses. If you’re still in the market for a home, carefully evaluate how much house you can afford to avoid overextending your budget.Alternatively, you can consider moving to a low cost of living location (LCOL) to keep your costs down.

The rate of return is an important factor that impacts your age of retirement. It is important to make sure to invest in ETFs or stocks that can provide a healthy rate of return, instead of keeping all your money in cash. One popular strategy is the Boglehead Investment Approach, which emphasizes low-cost, diversified funds.At the same time, it is wise to remember that the higher the return, the more the risk. So it becomes key to balance your asset allocations and manage risk effectively.

Medicare is typically available at 65, so if you retire earlier, you will have to think about options for health insurance and medical coverage. These options may include purchasing a healthcare plan directly from healthcare marketplace or working part-time in a job that provides coverage. Alternatively, if you have a spouse whose job provides insurance, you may want to join their health insurance plan.

Retirement accounts impose withdrawal penalties upto age 59 ½ . This means that you need to ensure you have sufficient liquid net worth in brokerage or other savings accounts to cover your living expenses until this age..

Starting age 50, you can make catch-up contributions on your retirements accounts and save an additional $7500 on your 401K and $1000 on your IRAs.

The IRS’ Rule of 55 allows you to withdraw funds from your current employer’s 401K if you have been laid off or quit your job when you turn 55. This does not include previous employer 401Ks unless they are rolled into your current employer’s 401K.

Retiring early, especially by age 55, is an achievable goal with the right planning and discipline. By focusing on your savings, investments, and lifestyle, you can pave the way to financial freedom. Remember, it’s not just about saving more but also about making smart financial decisions along the way.

To help you further in your journey, check out some of these helpful resources:

By taking small, consistent steps and leveraging all available resources, you’ll be well on your way to securing your financial future and enjoying an early retirement.

Start planning now and let your future self thank you!