How much house can I afford with a $100,000 salary?

Summary

A person with a salary of $100,000 can be eligible for a home value between $288,000 and $420,000. However, the exact home value depends on many factors and it is important to understand your full financial situation before deciding how much house to buy.

Here are some important factors to consider while thinking about home affordability:

- Your financial situation and lifestyle

- Debt-to-Income Ratios

- Interest Rate

- Credit Score

- Down Payment

Read our blog post How Much House Can I Afford to gain a detailed understanding of all the factors that influence home affordability.

In this post, we dive deep into finding out how to come up with a personalized home affordability number for an income of $100,000 tailored to one’s own financial situation.

Find out your personalized home affordability

Based on the standard debt/ income ratio of 36% typically used by lenders, you will be eligible for $383,000 home value. This assumes 30-year fixed interest rates of 6.72%, a down payment of $50,000 and monthly debt payments of $400.

What if you are a frugal person and can control your living expenses? In that case you may be able to afford a more expensive home. Or alternatively, if you tend to have a higher expense level, you may only be able to afford a lower home value.

Let us model out a couple of scenarios. To keep things simple, let us assume that you put away 10% of your gross income towards your 401K and make $400 in monthly car loan payments.

Let us consider a few different scenarios.

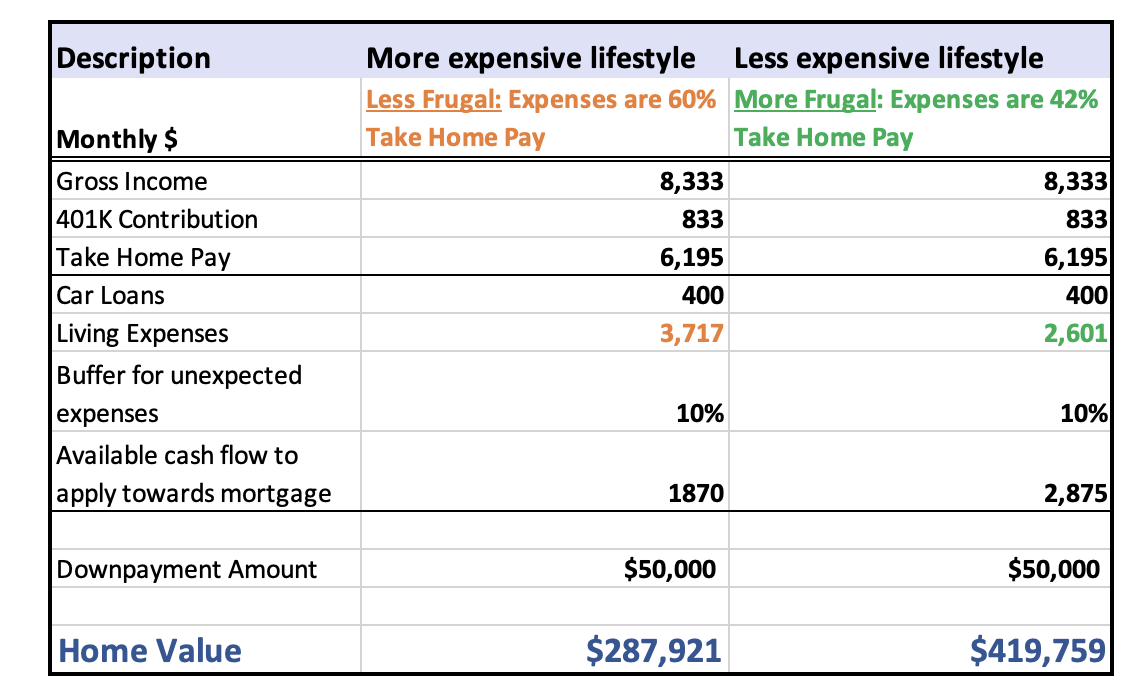

- Frugal lifestyle at 42% of take home Pay:If you are very frugal and your expenses are only 42% of Take Home Pay, you might be able to afford a home value of $419,000K. Of course, this may be constrained by the maximum that lenders will approve you for, but you know that you could perhaps be more aggressive in your choice of home.

- More expensive lifestyle with expenses at 60% of take home pay: You might find that you can only afford $287,000K of home value. In this case your options may be to find a less expensive home in a lower cost of living area. Or you could cut down your expenses.

What options do you have to buy a higher value home with a $100,000 salary?

Pay off existing loans

If you have existing loans, you can try to pay them off faster and get to a place where you can afford a more expensive home. For example, if you paid off your car loans in the scenario we described above, the home affordability (based on a debt/income ratio of 36%) would go upto $436,000 instead of the original $383,000.

Any bonus or extra savings can be used towards loan repayment. You can use the avalanche method and pay off the higher APR loans first. Or alternatively, you can pay off the smallest debt, move to the next bigger debt and so on. This is the snowball method.

Save more for downpayment

A higher down payment can increase the home value you can afford. By putting a higher downpayment on the table, you could also reduce the mortgage you have to take out, thereby reducing interest payments. Moreover , if you can make the down payment 20% of home value, you do not have to pay PMI charges. PMI is Private Mortgage Insurance and can run from 0.46% and 1.5% of the loan amount until the equity in the home reaches 20%.

Consider a lower cost of living location

One option may be to consider a lower cost of living option but be prepared to make tradeoffs. You may have to consider a neighborhood with a longer commute and without the amenities you want. Or people have also moved cities or states to be able to afford a better home with all the amenities and advantages they want, such as good schools or low crime.

Boost your income

A 20% higher income could increase your home affordability to $462,000 instead of the original $383,000. This may not be possible for everyone, but consider if there are ways to boost your income.

Could you get a raise or ask for that promotion? Or you could polish your resume to try to find a new job opportunity, although this might be harder when the economy is not great. Make sure to put your raise towards home budget or savings, and not towards a more expensive lifestyle.

Improve your credit score

Your credit score will determine the interest rates at which you get approved for your mortgage. The higher the credit score, the better mortgage rates you will get. So what factors determine your credit score?

Pay your bills consistently and on time. Have a low credit utilization rate and pay off your balances on time. Typically, good budgeting and debt management practices will not only help you get your finances to a better place, but also have the potential to boost your credit score.

Consider your lifestyles and tradeoffs

Think about the type of lifestyle you want. If you want to spend on travel or vacations, or if one parent wants to take time off to care for children, you may decide to buy a lower value home. Or alternatively, if you really value a more expensive home, you may want to cut back on other areas of your life. Instead of getting carried away by what other people are doing and trying to keep up with the Jones, it is more important to be thoughtful about what you and your family really want and trade off things that are less important.

At Planwell, we are building a fully automated AI financial planner and advisor to help you make super personalized financial decisions such as how much house you can afford, while considering your lifestyle, retirement goals and other key factors.

We will be launching the product very soon. Stay tuned for an update. In the meantime, check out our blog posts to help you plan your finances.

- How Much House Can I Afford: Review our blog post on all the factors that determine your home affordability.

- How to build a personal financial plan: Before you make a home purchase, make sure to build your personalized financial plan with our 10 step guide.

- How to Use AI Budget Calculators and Tools to Plan Your Finances: Take advantage of modern technology to plan your finances more effectively.

- 5 Common Money Mistakes to Avoid: Learn about the pitfalls that could derail your early retirement plans.

- 5 Overlooked Workplace Benefits That Can Save You Money: Maximize your work benefits to boost savings and well-being.

- 8 Financial Planning Tips for Young Adults: Start your financial planning journey early with these essential tips.

- How to Retire Early and Achieve Financial Independence: Deep dive into strategies that can help you retire early.

Related Posts

About

©2023 Planwell.io