Financial Planning Strategies For Doctors & Medical Professionals

Designed by Freepik

On the face of it, it may seem that doctors and physicians are in high paying professions and should be doing well financially. Primary care physicians earn an average of $277K and specialists earn about $394K.

However, despite these high salaries, physicians face some specific financial challenges due to a combination of factors:

- Doctors and physicians start their careers in their late twenties after at least 10 years of a medical education.

- They also tend to have huge medical school loans, with average doctor student loans being $200K.

- Moreover, physicians are in an extremely busy and high-stress profession and may not always have the time to be on top of their finances.

It is therefore important for doctors and medical professionals to plan their finances in a way that helps them achieve their financial goals while managing their time wisely.

Below are the top 5 strategies that doctors can use to plan their finances efficiently.

Debt Management

Given the high student loans, it is advisable for doctors to adopt a two-step approach for paying off their student loans:

Step 1: Determine whether you should pay off debt or invest

Since medical salaries are high, you may wonder whether you should use some of your salary and savings to pay down debt faster. Or should you invest in stocks or max out your 401K? Can you consider real estate investments?

The answer is: It depends.

You need to factor in interest rates on the student loans, the expected rates of return on stocks or other investments and tax savings, if you plan to invest in tax advantaged options. Additionally, you may also want to consider your own temperament - does having a high student loan balance make you anxious? Each of these is a key consideration for a physician aiming to plan their finances effectively.

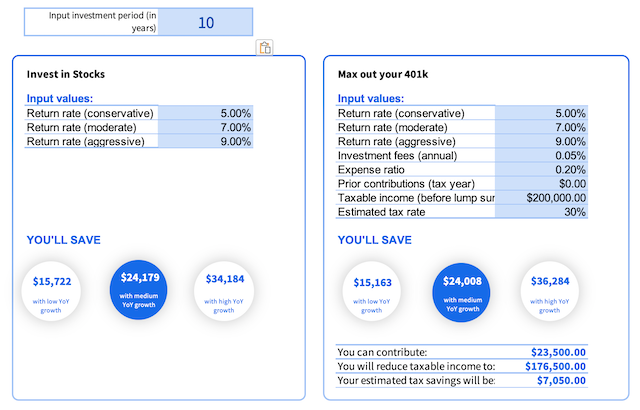

Consider the following scenario. Let us say you have $25,000 in savings from your salary that you can use to either pay off a portion of your student loan, or invest in stocks or 401K/ 403b. Let’s do the math.

Option 1: If you invest this $25,000 in stocks or 401K/ 403b

- If you invest in stocks, you can make a return of $24,179 over 10 years at a 7% rate of return.

- If you put this in your 401K, or 403b, you will earn $24,000 plus a tax saving of $7050 assuming a 30% tax rate.

Option 2: If you pay down debt:

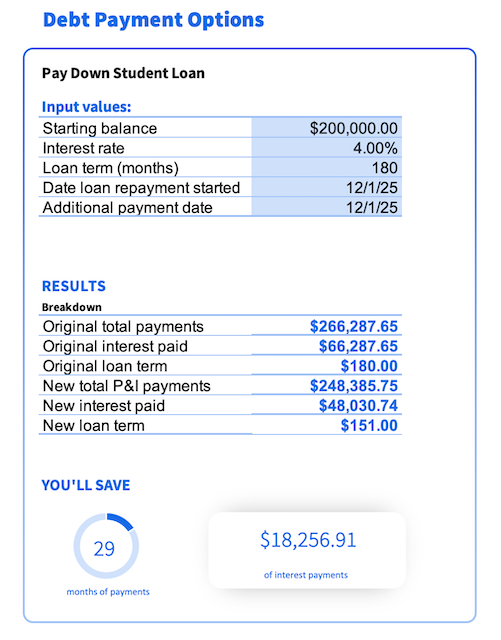

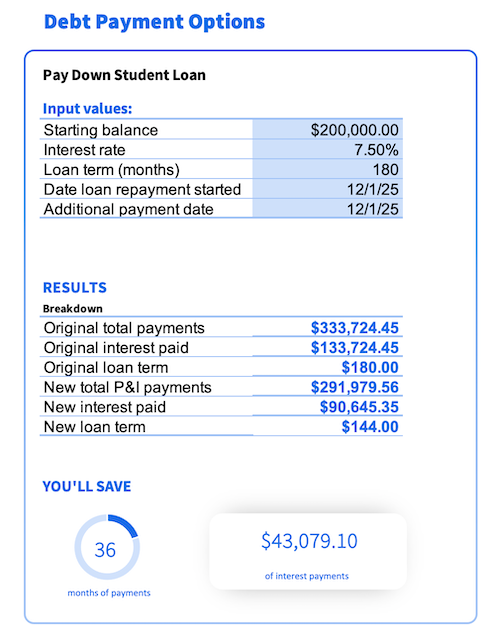

- If you pay down your $200K student loan at 7.5%, you will save $43,000.

On the other hand, if your student loan is at a lower interest rate of 4%, you will save only $18,256. In this case, it is better to use your $25,000 to invest in your 403b/ 401K or stocks since you will make a higher return on investing than paying off debt.

Therefore, you may want to pay off debt if it is 7.5%, but if the interest rate is low at 4%, you’d be better off maxing out your 401K or investing in stocks.

Step 2: Decide upon the right debt repayment strategies

After crunching the numbers if you decide that you want to focus on debt repayment, there are a couple of strategies you could consider to pay down debt faster.

Debt avalanche method

In this method, you pay off the debt with the highest interest rate first. Then you pay off the debt with the next highest interest rate, and so on. Of course, you’d have to pay off the minimums on all other debts, but if you have any excess money, you put it towards the highest interest rate debt. This helps reduce the interest payments and helps pay off debts faster.

Debt snowball method

In this method, you pay off the smallest value debt first. Then tackle the next small debt, and so on. This is a good motivator and morale booster since you can see debts being paid off, so it may work for people who want a psychological boost while paying off debts.

Retirement planning

Max out your retirement contributions

Doctors typically have access to 401Ks or if they work for non-profits, they have access to 403(b) retirement options. Investing in pre-tax retirement options helps reduce taxable income and save on taxes.

Many physicians also can save pre-tax dollars in employer sponsored 457b accounts. The limit for 2025 is $23,500. So if you max out both the 401K/ 403(b) and 457b, you can save twice as much at $46,000. This helps you catch up on your retirement savings, even if you have a late start to your career.

Review our blog post on Backdoor Roth IRA strategy.

HSAs

An HSA account is a tax advantaged savings and investment account used with a high deductible health plan (HDHP). It is used for healthcare expenses.

It is triple tax advantaged for the following reasons:

1. You contribute pre-tax dollars, thereby lowering your taxable income.

2. You can invest some or all of the funds in your HSA. This amount grows tax free, meaning that you do not pay taxes on investment gains.

3. If you withdraw the money in the HSA for qualified healthcare expenses, then you do not pay taxes on these withdrawals.

- Note that you can make withdrawals for non-healthcare purposes in retirement, but will need to pay taxes on such withdrawals.

However, since HSAs are paired with a High Deductible Health Plan, it means that it is not a good option for people who need medical care frequently. The deductibles and out-of -pocket maximums are higher than PPOs or HMOs, so if you or your family needs frequent medical care, you will end up spending a lot of healthcare costs out-of-pocket.

Backdoor Roth IRAs

Physician incomes are usually too high to contribute to standard Roth IRAs, which have a modified adjusted gross income (MAGI) limit of $161,000 for single filers and $254,000 for married filing jointly. However, physicians who exceed these income limits still have the option to take advantage of the Backdoor Roth IRA. First contribute post-tax dollars to a regular IRA and then make a Roth conversion to move these funds to a Roth IRA.

Here is how you can max out your retirement contributions:

- 401K/ 403b: $23,500

- Roth IRA (via Roth conversion): $7000

- Mega Backdoor Roth: If your employer plan allows after-tax contributions, you can save upto $69,000 (including the 401K, employer match and additional amount adding upto $69,000).

- 457b: $23,500

- HSA: If you qualify for an HDHP and do not need frequent medical care in the current time.

Insurance and risk management: Malpractice insurance, life and disability insurance

Malpractice Insurance

According to data from the American Medical Association (AMA), in 2022, 31.2 percent of physicians reported that they had been sued in their careers to date. Therefore malpractice insurance is very important for doctors to protect themselves against litigation. Malpractice insurance provides coverage for different types of expenses such as lawyer and attorney costs, settlement amounts, damages and other costs associated with medical litigation and will protect doctors’ personal assets in the case of litigation.

It is estimated that liability premiums are about 3.2% of physician annual income. Hospitals generally provide malpractice insurance to doctors, but doctors practicing privately may have to buy their own insurance.

Disability insurance

Doctors would do well to protect themselves in case they become injured or unwell and this affects their earning potential. There are 2 types of disability insurance:

Short term disability

- Pays for a period of 3-24 months

- Commences paying soon after injury

Explore whether your workplace already offers this benefit. Alternatively if you have an emergency fund or cushion to tide you in the short term, you may not need this as much.

Long term disability

- Does not pay immediately but commences paying after 3-24 months.

- It will pay a benefit each month until retirement age.

- This policy protects you in case you lose your earning ability permanently or for the long term.

Life insurance

Since doctors make a high salary, they should make sure their family is protected in case the unthinkable should happen. This is where life insurance comes in. Life insurance should cover the following: replace the income from the main breadwinner, factor in the cost of housing and mortgage, childcare and college costs for kids.

Investing

If you are very busy with your medical career, it may be best to use the Boglehead approach to investing. Passive investing in low cost index funds, long term focus , investing in low investment fees funds, asset diversification and reducing volatility with prudent risk management. Passive investing requires less management and lower frequency transactions and therefore is associated with low fees and low transaction costs.

(5) Real estate investing

Once you have taken care of all the above options, you can evaluate putting any surplus funds into real estate investing. Note that real estate investing is not for everyone. You need to think about whether you are ready to be a landlord temperamentally.

For real estate investing, it is important to evaluate key metrics such as the Internal Rate of Return, Profit from rent & future sales and Breakeven Rent. Make sure to factor in all obvious and hidden costs, including vacancy rates, maintenance and property taxes..

Conclusion

Doctors tend to have high salaries but also constraints such as high student loan debt and starting their careers later than people in other professions. Therefore, their financial planning requires a mix of strategies:

(1) Making the decision to pay down debt vs investing,

(2) Maxing out retirement options, including 403b/ 401K, HSA, Roth conversion, Mega backdoor Roth, and 457b.

(3) Buying insurance, including malpractice, disability and life insurance

(4) Adopting a practical and time-efficient investing approach such as the Boglehead approach to investing

(5) Evaluating whether real estate is a good fit given one’s finances and temperament.

At Planwell, we are building a fully automated AI financial planner and advisor to help doctors and medical professionals make super personalized financial decisions such as how to retire early and achieve financial independence & how much house you can afford, while considering your lifestyle, retirement goals and other key factors.

We will be launching the product very soon. Stay tuned for an update. In the meantime, check out our blog posts to help you plan your finances.

- Backdoor Roth IRA Process: Learn more about the backdoor Roth IRA process.

- 5 Overlooked Workplace Benefits: Lesser known workplace benefits that can be super useful and help save a lot of money.

- How to build a personal financial plan: Build your personalized financial plan with our 10 step guide.

- How to Use AI Budget Calculators and Tools to Plan Your Finances: Take advantage of our free FIRE calculator to plan your finances more effectively.

- 5 Common Money Mistakes to Avoid: Learn about the pitfalls that could derail your early retirement plans.

Related Posts

About

©2023 Planwell.io