Image by vectorjuice on Freepik

You have heard of Lean FIRE and Fat FIRE. Now let’s look at Chubby FIRE, the Goldilocks version of FIRE– neither too lean nor too fat, but just right.

Chubby FIRE involves a moderately affluent lifestyle which is not as extravagant as Fat FIRE but is also not super frugal. FIRE involves becoming financially independent and retiring early, which leaves open a wide range of options. Chubby FIRE enthusiasts can count on an enjoyable retirement lifestyle, including some travel, dining out, and generally enjoying a nice standard of living without having to scrimp and pinch the pennies. Think of Chubby FIRE as an upper middle-class FIRE lifestyle, but not a wealthy lifestyle.

With Chubby FIRE, you can maintain a comfortable retirement lifestyle and not give up any of the regular things you are accustomed to, such as dining out, travel, or entertainment. You do, of course, have to follow a sensible budget that ensures that your savings rate is high without having to scrimp and save on every penny. Even better if your home mortgage and other debt is paid off before retirement, leaving you free to enjoy all your assets without worrying about liabilities.

You can supplement your retirement income with side income or real estate investing. This ensures that you are more comfortably set up in retirement and you de-risk your retirement further.

Chubby FIRE is ideal for people who have a professional or salaried career and making a good income, but are not super wealthy. Such a career will help you achieve a healthy savings rate.

In keeping with the theme of balance, the Chubby FIRE investment approach is balanced and disciplined – neither too aggressive nor too conservative. Invest in low fees investment options while ensuring adequate diversification, tax planning and risk management.

To achieve Chubby FIRE, it is important to save a healthy proportion of one’s income but it is not necessary to live super frugally before retirement. Budgeting is key, to ensure that you spend on things that are really important to you but without being extravagant.

Chubby FIRE focuses on having a comfortable, upper middle class lifestyle, both before and during retirement. This ensures that you do not have to be ultra frugal and subsist on ramen noodles. A healthy balance is maintained in one’s lifestyle and spending, while also ensuring that there is disciplined saving and budgeting.

It is important to understand that investing in stocks or real estate is important to grow one’s assets and build long term wealth. However, with Chubby FIRE, you avoid taking on excessive investment and focus on a balanced and disciplined approach to growing assets and wealth.

Also see our blog post on Boglehead investing.

While you do not need to have as much wealth as in Fat FIRE, Chubby FIRE still involves having a professional or high paying career with a high savings rate. Therefore, it may be out of the reach of many people who are not focused on higher paying career choices. Moreover many people may prefer to be in less demanding or stressful careers and yet achieve FIRE by living frugally.

Many high earners can become tempted by the HENRY (High Earners, Not Rich Yet) lifestyle. This means they have a high income but are low on assets due to a high level of spending. While people may have good intentions to save a good portion of their income, an upper middle class income can cause spending to get out of control with more expensive housing, fancy cars or private schools. You need to make a very conscious effort to avoid lifestyle creep.

If you intend to retire early, you need to make sure that you will have access to health insurance in your retirement years.

Make a sensible budget that enables you to save a good proportion of your income while also enjoying life in the moment. A good approach here is to curtail spending on most things while splurging on a very small number of things that you enjoy the most. Some people may wish to spend money on their kids, or on travel or dining out with friends. But save aggressively on all other things that you do not care about. This enables you to achieve a high savings rate while enjoying the things you love.

Invest your savings using a disciplined, long-term investing approach, such as Boglehead investing. This involves mostly passive investing in low cost index funds and buying and holding for the long term. Make sure to diversify your assets and reduce volatility and manage risk.

After retirement, consider whether you want to move to low cost of living(LCOL) locations. This will help you reduce your retirement spending while maintaining a good quality lifestyle. Since the housing costs in retirement will be lower, you may even be able to retire early by moving to a LCOL.

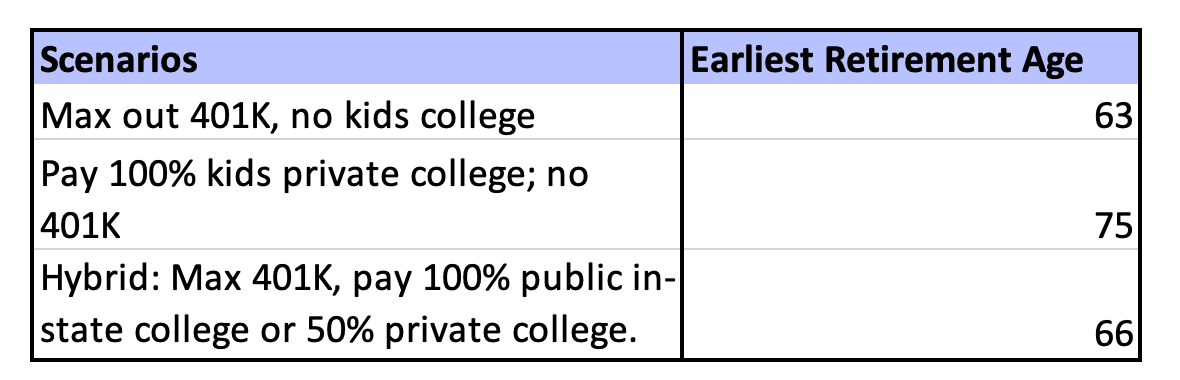

The Planwell financial planning app helps you plan for your Chubby FIRE goal in just a few minutes. Input your basic financial details and your planned retirement lifestyle. Planwell provides an instant financial plan and tells you the earliest age that you can achieve your chubby FIRE retirement.

Both Chubby FIRE and Fat FIRE involve an affluent lifestyle before and during retirement. But Chubby FIRE involves a more balanced upper middle-class lifestyle. Fat FIRE, on the other hand, allows for an extravagant lifestyle after retirement and building significant wealth to be able to retire early. Moreover, one might invest more aggressively (and thereby accrue more risk) with Fat Fire, in order to earn higher returns. But with Chubby FIRE, we focus on a more balanced investing approach and optimize for both investment growth and risk management.

Barista FIRE allows one to retire early and afford a more comfortable lifestyle in retirement because people plan to work at least part time in retirement. With Chubby FIRE, there is no expectation to work in retirement, and the idea is to have enough saved to be able to retire and afford a comfortable lifestyle. Also, with Barista FIRE, the part time job may come with health insurance, thereby reducing healthcare related risks in retirement. But with Chubby FIRE, we have to plan for health insurance.

The regular or standard FIRE involves living somewhat frugally before and during retirement. But with Chubby FIRE, the goal is to live a more comfortable lifestyle.

Moreover, Chubby FIRE is typically for upper middle-class people who hold salaried professional jobs before retirement. But the standard FIRE is accessible to everyone, not just upper middle-class folks.

Chubby FIRE is a happy medium between the extreme frugality of Lean FIRE and the affluence of Fat FIRE. It typically works for people working in jobs that afford an upper middle-class salary and lifestyle. People considering Chubby FIRE need to do careful budgeting and planning but do not need to pinch pennies. They can adopt a balanced investment strategy that helps them grow assets without undue risk.

Planwell can help you plan for Chubby FIRE with our fully automated financial planning tool.