Can I afford a child?

A step-by-step guide for planning finances for a new child.

Becoming a parent is a time of great excitement and anticipation. But this is also a good time to think about your finances and make sure you are financially well set up for a new child – whether it is your first child or second.

It is estimated that total average family expenditures on a child born in 2015 to a middle-class family with two children, adjusted for higher expected future inflation, would be $310,605 (estimates from the Brooking institute ). This can seem pretty financially challenging, which is why we put together this step-by-step primer to help you plan finances for a new baby and determine whether you can afford a child—or even a second child.

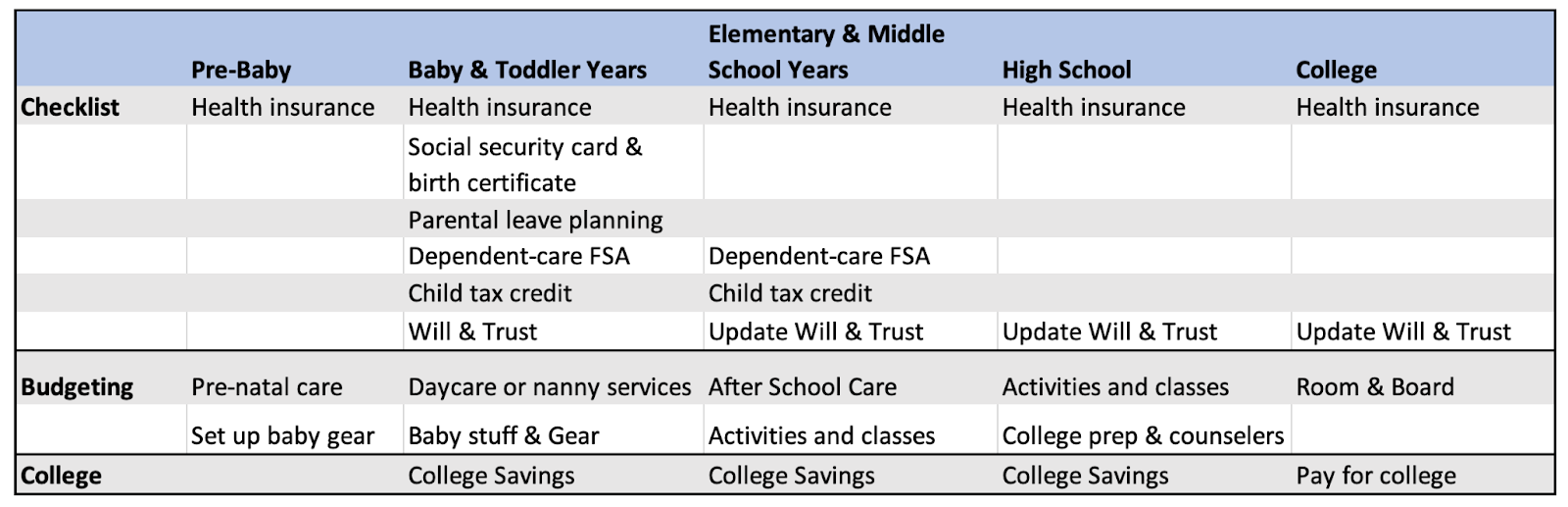

Here is a quick overview of all the major things you need to be planning for. Let’s break it down by different stages of the baby’s birth and growing years.

Before and soon after birth

The process of planning finances for a new baby starts even before birth. These are many things you need to have in place even at this early stage.

Health insurance

Plan for both prenatal care and post-delivery medical care. Evaluate your employer’s health insurance plan and understand how much will be covered by insurance and how much you might have to pay out-of-pocket. You may need to update your Health Savings Accounts (HSA) based on anticipated medical expenses.

Make sure to add the baby to your or your spouse/ partner’s health insurance plan within the stipulated period after birth, typically 30 days.

Parental leave planning

Understand your company’s parental leave policy and how much leave is covered by the company. Also understand the Family and Medical Leave Act (FMLA) benefits and see if it is applicable for you. The FMLA can provide up to 12 weeks of unpaid job protected leave in a year for specific family and medical reasons. It ensures that health insurance coverage is maintained during this period. Many states also have established paid family leave systems that provide parental and family caregiving leave and temporary disability insurance to cover paid personal medical leave.

Life insurance and beneficiary designation

If you have dependents, you should have a life insurance plan in place to ensure that the child or other survivors are taken care of if the unthinkable happens. Many employers offer life insurance benefits. You can evaluate these to see if the benefits will cover your family in case of death, or whether you want to increase this amount through your employer or buy life insurance separately. You may also want to add your child as a beneficiary after birth.

Social security card and birth certificate

Hospitals have put in place streamlined processes to order the baby’s social security card and birth certificate soon after birth. This saves a lot of time and effort later on when you might be busy with taking care of the baby.

Baby and toddler years

Dependent-care flexible spending account (FSA)

The Dependent Care FSA is used to pay for childcare expenses if you and/ or your spouse work or attend school full time. It is an employer-sponsored account and you can deposit pre-tax dollars to help pay for caregiving expenses for children under age 13. One thing to remember: this is a ‘use-it-or-lose-it’ benefit. The money in your account does not roll over into the next year if you end up not using it in the current year. So make sure to plan and estimate how much you will be spending for childcare in the current tax year.

Child and dependent care tax credit

This is a tax credit that you can claim on federal taxes if you have spent money on qualified childcare expenses while you work. The maximum credit you can claim on one qualifying child is $3000 and for two or more children, the maximum is $6000. The actual value of the tax credit you will get is dependent on your adjusted gross income (AGI) and the amount of qualifying expenses that you have incurred.

Will and estate planning

It is important to have a will and estate plan in place to make sure that the child’s well-being is secured in case of untimely death of the parents. You should designate a guardian to raise the child instead of leaving it to a court to designate a guardian. You should also stipulate in the will how your assets will be allocated to your children and spouse. You can also designate a guardian to administer the estate until the child reaches legal age. This guardian can be different from the person nominated to take care of the child’s upbringing.

Budgeting for baby

Childcare is possibly the biggest expense for new parents and it is wise to start researching options that fit your criteria and budget as soon as possible. Home-based daycare may be less expensive than childcare centers or nanny services. Childcare costs are highest for infants and tend to go down with time.

Other major expense categories for babies and toddlers are diapers, car seats, baby clothes, toys, bottles, formulas, crib, baby monitor and so on. While it is hard to do without many of these, it is important to keep in mind that there is way too much hype and marketing and it is not really necessary to splurge on the most expensive products. In fact, you could also consider buying used products wherever possible.

School & College Years

School Year Budgeting

As kids enter school years, expenses can reduce quite a bit especially if you opt for public schools. However, you may now have new expenses such as kids’ classes and activities. You may also have to think about after-school care if both of the child’s parents are working.

College Savings

You may want to start planning for college expenses sooner rather than later. The earlier you start saving for college, the lesser you have to save due to the power of compounding. Check out our college saving calculator to plan your savings.

Conclusion

Deciding whether you can afford a child—or a second child—requires careful financial planning and thoughtful consideration of your current and future expenses. By evaluating your health insurance, childcare costs, and savings strategies, you can better understand how prepared you are for the financial responsibilities that come with growing your family.

To help you along the way, here are some additional resources to deepen your understanding of personal finance and make informed decisions:

- 5 Common Money Mistakes to Avoid: Learn about common financial missteps that could affect your ability to afford a child.

- 5 Overlooked Workplace Benefits That Can Save You Money: Maximize your workplace benefits to boost your savings for future family needs.

- 8 Financial Planning Tips for Young Adults: Essential tips for building a strong financial foundation before starting or expanding your family.

- College Savings Calculator: Start planning for long-term expenses like college, which can impact your decision to have another child.

- How Much House Can I Afford?: Ensure that your housing situation supports your growing family without stretching your finances too thin.

- How to Build a Personal Financial Plan: A 10-Step Guide: Learn how to create a comprehensive financial plan that takes into account the costs of raising a child.

- How to Use AI Budget Calculators and Tools to Plan Your Finances: Leverage modern tools to help manage your finances effectively and determine if you're financially ready for a child.

By using these resources and planning ahead, you’ll be in a much stronger position to confidently answer the question, “Can I afford a child?” and make the best financial decisions for your family’s future.

Photo by Bermix Studio on Unsplash

Related Posts

About

©2023 Planwell.io