Welcome to the Planwell blog! At Planwell, our mission is to help people make good financial decisions and live their best life.

Our first blog post highlights some very common money mistakes that are made by even the savviest people. And no, I am not talking about spending $5 on coffee. The mistakes I highlight below are much more consequential but also can be remedied with a little bit of extra attention.

Let’s get into it, shall we?

Mistake 1: Missing out on Backdoor Roth Conversion

The Backdoor Roth is a tax strategy for high earners who cannot contribute to a regular Roth IRA due to income limits. The Roth IRA allows people to contribute after-tax dollars to an Individual Retirement Account (IRA), and not pay taxes on withdrawals after age 59 ½. However, there are income limits for saving money in a regular Roth account which prevent many professionals in high earning careers from taking advantage of the tax benefits of a Roth IRA.

According to the IRS website, the income phase-out range in 2024 for taxpayers making contributions to a Roth IRA is between $146,000 and $161,000 for singles and heads of household. For married couples filing jointly, the income phase-out range is between $230,000 and $240,000.

The solution is to use the Backdoor Roth strategy which allows high earners to contribute money to a Roth IRA via a 2-step process. You should first contribute money to an IRA and then roll over this money to a Roth IRA. For 2024 you can contribute upto $7000 with an additional $1000 for people 50 and above.

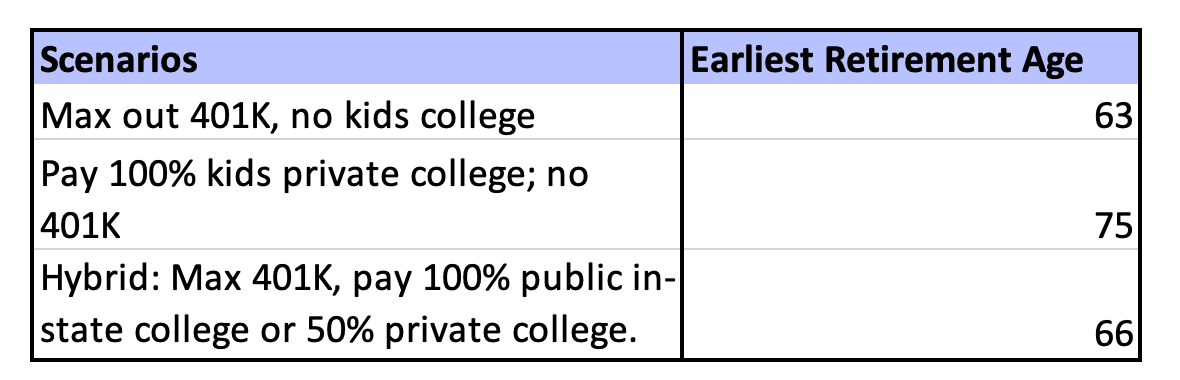

Mistake 2: Not maxing out 401K

This sounds very obvious, but you’d be surprised how many people do not max out their 401K even when they have enough money to save. Sometimes people may instead choose to pay down loans or invest in the stock markets, which are good things in general. But it is advisable to do the math and analyze the tax savings obtainable by maxing out 401K versus paying down loans or investing in the markets before you make this decision. Our Payoff calculator spreadsheet (available on Etsy) can help you do the math easily and make a well informed decision.

Mistake 3: Holding too much cash

In general, it is advised to hold 6 to 12 months’ worth of expenses as emergency cash savings. But you’d be surprised how many people hold a lot more than that in cash. Sometimes this is because people want the security and comfort of being able to access cash easily. Other people may just forget that they have accumulated a lot of money in their accounts and end up missing out on the gains they may get from investing this money.

Pro- tip: A smart move is to set up a monthly auto-transfer from your bank account to an investment account. This ensures that you are investing in the markets even if you are busy with your career and not paying attention to your money constantly.

Mistake 4: Not having enough life and disability insurance

Nobody likes to think of scenarios that make life and disability insurance useful. But that should not preclude us from making sure that we have enough life and disability insurance to tide us over during hard situations.

Mistake 5: Not doing Estate Planning

It is very important to ensure that you have adequate estate planning that covers the following requirements:

Pro-tip: Check to see if you can avail of legal services through employer benefits. This can significantly reduce the legal costs around estate planning.

Photo by Alexander Grey on Unsplash